As mentioned in the first posting, wellness programs must be analyzed under a myriad of laws and regulations. This post will discuss generally the wellness program landscape in light of the Americans with Disabilities Act (ADA)/Americans with Disabilities Act Amendments Act (ADAAA), the Genetic Information Non-Discrimination Act (GINA), the Patient Protection and Affordable Care Act (PPACA), and the Health Insurance Portability and Accountability Act of 1996 (HIPAA) and the Nondiscrimination Regulations. This is a 30,000-foot overview of laws and regulations that are in need of microscopic scrutiny when applying them to a wellness program.

As mentioned in the first posting, wellness programs must be analyzed under a myriad of laws and regulations. This post will discuss generally the wellness program landscape in light of the Americans with Disabilities Act (ADA)/Americans with Disabilities Act Amendments Act (ADAAA), the Genetic Information Non-Discrimination Act (GINA), the Patient Protection and Affordable Care Act (PPACA), and the Health Insurance Portability and Accountability Act of 1996 (HIPAA) and the Nondiscrimination Regulations. This is a 30,000-foot overview of laws and regulations that are in need of microscopic scrutiny when applying them to a wellness program.

ADA/ADAAA

The ADA/ADAAA generally prohibits discrimination in employment against a qualified individual on the basis of a disability in regard to employee compensation and other terms, conditions, and privileges of employment. Further is a prohibition from requiring a medical examination and making inquiries of an employee as to whether he or she has a disability, or as to the nature or severity of a disability, unless such examination or inquiry is shown to be job-related and consistent with business necessity.

However, there is a statutory safe harbor that exempts certain insurance plans from the ADA’s general prohibitions. The “benefit plan exception” states that the ADA shall not be construed as prohibiting an employer from establishing, sponsoring, observing, or administering the terms of a bona fide benefit plan that are based on underwriting risks, classifying risks, or administering such risks that are based on, or not inconsistent with, state law or where the plan is not subject to state law (a self-funded benefit plan) so long as the exemption is not used as a subterfuge for discrimination. As such, voluntary medical examinations and/or histories, which are part of a group wellness program, are permissible so long as strict confidential processes are followed.

What does it mean to be voluntary? There is no short answer, but the abbreviated answer is that a wellness program may be voluntary if the employer neither requires participation, nor penalizes employees who do not participate. The U.S. Equal Employment Opportunity Commission (EEOC) once posited that a health reimbursement arrangement (HRA) administered as part of a wellness program that meets the incentive limitations of HIPAA wellness regulations – no more than a (then) 20% reward – would be deemed voluntary and would not violate the ADA. Unfortunately, this portion of the opinion letter was withdrawn because it was outside the scope of the request. The position currently held by the EEOC is that an incentive is a veiled penalty, which, in essence, makes the program involuntary and, thus, violates the ADA. However, this is in conflict with the “benefit plan exception,” noted above.

GINA

Generally, GINA prohibits both the acquisition of genetic information as well as the use of genetic information by employers in employment decisions. As it applies to group health plans, Title I prohibits discrimination in health insurance premiums based on genetic information and places limitations on genetic testing and the collection of genetic information. Title II prohibits the use of genetic information in the employment context, restricts employers from requesting, requiring, or purchasing genetic information, and strictly limits employers from disclosing genetic information.

In general, Title II limits the conditions under which an employer might lawfully collect genetic information pursuant to an employer-sponsored wellness program and it requires those employers to follow strict privacy and confidentiality mandates. Under GINA, it is unlawful for an employer to request, require, or purchase genetic information with respect to an employee or an employee’s family member. There is an exception if the information is part of a wellness program, subject to strict adherence of the following three requirements:

- The employee provides prior, knowing, voluntary, and written authorization;

- Only the employee (or family member if the family member is receiving genetic services) and the licensed health care professional, or board certified genetic counselor involved in providing such services, receive individually identifiable information concerning the results of such services; and

- Any individually identifiable genetic information provided in connection with the services is only available for purposes of such services and shall not be disclosed to the employer except in aggregate terms that do not disclose the identity of specific employees.

Again, what does it mean to be voluntary? In the preamble to the 2010 final regulations implementing Title II, the EEOC concluded that a wellness program is voluntary if the program neither requires participation, nor penalizes employees for non-participation. The EEOC concluded that it would not violate Title II for an employer to offer individuals an inducement for completing an HRA that includes questions about family medical history, or other genetic information, as long as the employer specifically identifies those questions and makes clear, in language reasonably likely to be understood by those completing the HRA, that the individual need not answer the questions that request genetic information in order to receive the inducement. The EEOC specifically declined to take the approach taken in HIPAA regulations – no more than a (then) 20% reward – and, instead, added that adherence to Title II of GINA does not guarantee adherence to Title I of GINA, ADA, or HIPAA.

HIPAA and PPACA

The general rule pursuant to HIPAA nondiscrimination provisions is that a plan or issuer is prohibited from charging similarly situated individuals different premiums or contributions on the basis of a “health factor.” However, there is an exception to the general rule if the reward, i.e., premium discount, is based on participation in a program reasonably designed to promote health or prevent disease, i.e., a “wellness program.”

When analyzing a wellness program under PPACA and HIPAA, the first step is to determine whether the wellness program – or, as it may be the case, which part of the wellness program – is “participatory” or “health-contingent.” Participatory wellness programs are not required to follow HIPAA nondiscrimination provisions, discussed below. However, and to the point of this blog series, participatory (and health-contingent) wellness programs should be reviewed and scrutinized against the provisions of GINA, ADA, the Employee Retirement Income Security Act (ERISA), Internal Revenue Code (IRC), and other federal and state laws.

Participatory wellness programs are defined under HIPAA nondiscrimination final regulations as programs that either do not provide a reward, or do not include any conditions for obtaining a reward that are based on an individual satisfying a standard that is related to a health factor. Examples include a program that reimburses employees for all or part of the cost of membership in a fitness center, a diagnostic testing program that provides a reward for participation and does not base any part of the reward on outcomes, and a program that provides a reward to employees for attending a monthly, no-cost health education seminar.

If the wellness program, or a piece of the wellness program, is participatory, it does not have to follow HIPAA nondiscrimination regulations. However, if the wellness program, or a portion thereof, is health-contingent, then the program must be analyzed pursuant to HIPAA nondiscrimination regulations.

HIPAA Nondiscrimination Provisions and the Wellness Program Exception

Health-contingent wellness programs, in contrast to participatory programs, require an individual to satisfy a standard related to a health factor to obtain a reward or require an individual to undertake more than a similarly situated individual based on a health factor in order to obtain the same reward. The standard may be performing or completing an activity relating to a health factor, or it may be attaining or maintaining a specific health outcome. The final regulations further subdivided health-contingent programs into (1) activity-only wellness programs, and (2) outcome-based wellness programs. While there are some differences, both types are permissible only if the program adheres to the five prongs:

- Be reasonably designed to promote health or prevent disease (the same rules apply to activity-only and outcome-based programs);

- Give employees a chance to qualify for the incentive at least once a year (the same rules apply to activity-only and outcome-based programs);

- Cap the reward or penalty at 50% of the total cost of coverage for avoiding tobacco and at 30% for all other types of wellness incentives (the same rules apply to activity-only and outcome-based programs);

- Provide an alternative way to qualify for the incentive for those who have medical conditions (different rules apply to activity-only and outcome-based programs); and

- Describe the availability of the alternative method of qualifying for the incentive in written program materials (the same rules apply to activity-only and outcome-based programs).

These rules set forth criteria for an affirmative defense that can be used by plans and issuers in response to a claim that the plan or issuer discriminated under HIPAA nondiscrimination provisions.

This is not the end…

The above is merely a general overview of the innate tension created by conflicting regulations, compounded by the lack of guidance from the commission, which is confronting concerned employers who have chosen to be proactive in combating the costs of health care and improving consumers’ lives. The next part of the series will discuss the movements in the courts, the backlash felt by the EEOC, and steps employers should take.

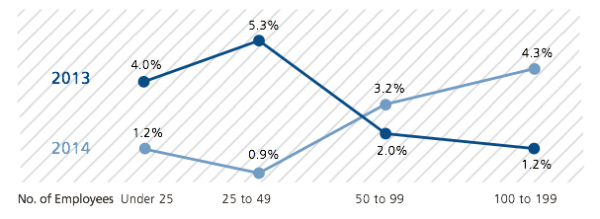

For more data on wellness programs and other plan design trends, download the 2014 Health Plan Executive Summary. This survey – which has been conducted every year since 2005 – is the nation’s largest health plan survey and provides more accurate benchmarking data than any other source in the industry. You can contact a UBA Partner Firm for a customized benchmark report based on industry, region and business size.

The Department of Health and Human Services (HHS) has issued its proposed Benefit and Payment Parameters for 2016. While these amounts and dates are not yet final, they may be of help for planning purposes. At this time, HHS expects:

The Department of Health and Human Services (HHS) has issued its proposed Benefit and Payment Parameters for 2016. While these amounts and dates are not yet final, they may be of help for planning purposes. At this time, HHS expects:

The IRS has released final regulations that address how wellness incentives or penalties, contributions to a health reimbursement arrangement, and employer contributions to a Section 125 plan are applied to determine affordability. While these regulations were issued in connection with the individual shared responsibility requirement (also called the individual mandate), the agencies said that they expect to use the same approach when determining affordability for purposes of eligibility for the premium tax credit and the employer-shared responsibility/play or pay requirements.

The IRS has released final regulations that address how wellness incentives or penalties, contributions to a health reimbursement arrangement, and employer contributions to a Section 125 plan are applied to determine affordability. While these regulations were issued in connection with the individual shared responsibility requirement (also called the individual mandate), the agencies said that they expect to use the same approach when determining affordability for purposes of eligibility for the premium tax credit and the employer-shared responsibility/play or pay requirements.

Premium tax credits are only available to individuals who obtain health coverage through a Marketplace. A dispute has arisen as to whether the IRS has the ability to interpret PPACA to allow the subsidy to individuals who obtain coverage through any Marketplace, or whether the language of PPACA limits eligibility to those who have obtained coverage through a state Marketplace. The U.S. Supreme Court has agreed to rule on whether premium tax credits may only be available to individuals who receive tax subsidies as a result of being enrolled in a state exchange. In the meantime, the IRS has

Premium tax credits are only available to individuals who obtain health coverage through a Marketplace. A dispute has arisen as to whether the IRS has the ability to interpret PPACA to allow the subsidy to individuals who obtain coverage through any Marketplace, or whether the language of PPACA limits eligibility to those who have obtained coverage through a state Marketplace. The U.S. Supreme Court has agreed to rule on whether premium tax credits may only be available to individuals who receive tax subsidies as a result of being enrolled in a state exchange. In the meantime, the IRS has

The employer-shared responsibility (“play or pay”) requirements do not apply to small employers and have been delayed until 2016 for most mid-sized employers. This raises the question – what exactly is included in the play or pay requirement, which a small employer may be able to ignore and that mid-size employer may not need to meet until later?

The employer-shared responsibility (“play or pay”) requirements do not apply to small employers and have been delayed until 2016 for most mid-sized employers. This raises the question – what exactly is included in the play or pay requirement, which a small employer may be able to ignore and that mid-size employer may not need to meet until later?